Ever found yourself pondering the financial freedom of a retired Major League Baseball (MLB) player, wondering if that Hall of Fame plaque might also herald substantial monthly income? The thought invariably circles back to the “pension” – a word that often conjures images of a secure, steady stream of retirement dollars. But how much are we really talking about? While every retired star has a unique story, understanding the mechanics behind these pensions, and consequently, their actual payout, involves navigating a structure built decades ago with specific provisions. Let’s peel back the layers to see just what grace retired ballplayers’ bank accounts receive from this particular source of income.

The Essence of the Plan: What Exactly Is an MLB Pension?

The term “pension” itself hints at its nature – a defined benefit plan, distinct from the more common 401(k) or variable savings accounts many of us understand today. It’s a contract, essentially an agreement established over half a century ago, promising financial support to qualifying former players based on factors like their years of service (or credited service) and their final salary in the Major Leagues. This isn’t a pot of money to be drawn from at will; it’s calculation-based, offering a predictable, lifetime income stream post-retirement.

The Pillars of Funding: How Was It Supposed to Work?

Historically, the funding mechanism for these pensions faced criticism – much like today’s debates around Social Security. Before the plan became stabilized (a process completed largely through collective bargaining agreements later in the century), funding depended significantly on Major League Baseball’s revenues. Payments made by players were relatively minimal until the plan faced insolvency concerns in the 1980s. This necessitated a seismic shift. MLB, the players’ association (now the MLBPA), and a consortium of team owners banded together to establish a dedicated funding pool. This pool is meticulously funded by annual assessments levied on the revenues generated by the sport itself, guaranteeing the pension fund’s solvency regardless of individual player salaries or the league’s fluctuating fortunes.

The Calculation Conundrum: Determining the Monthly Check

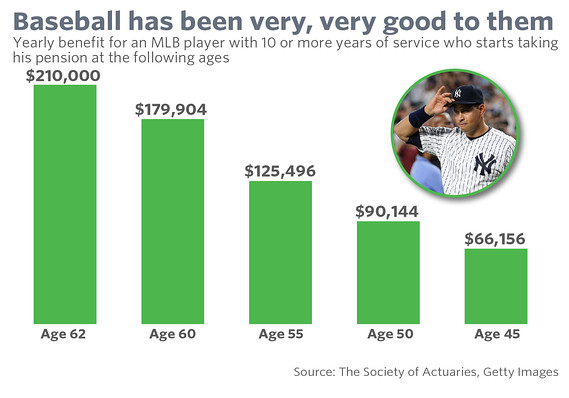

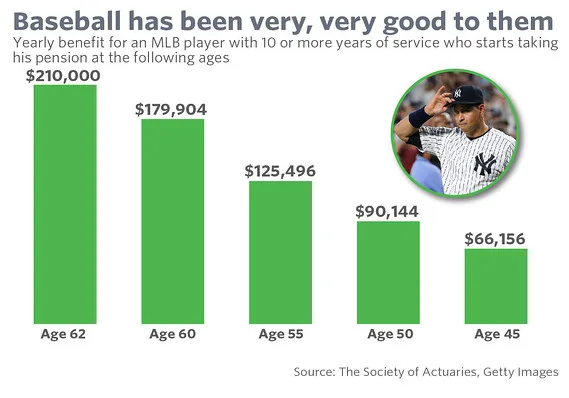

So, how does one’s share get figured out? The core formula translates credited service into percentage points. Each year (or fraction thereof) of Major League service contributes x% to the player’s pension. But “creditable service,” as defined by the plan (and potentially updated by recent agreements), can vary, sometimes acknowledging military service during wartime. Importantly, the player’s Final Average Monthly Income (FAMI) – essentially their Major League salary in their final year – becomes the base upon which these percentage points are applied. The result is a defined monthly benefit. There’s little wiggle room here. For instance, an 18-year service player might receive 1.5% for each year up to that point (or a similar structure, depending on the specific agreement period), a portion of their final salary. This calculation aims for consistency among peers, though the resulting pension amounts vary significantly based on playing duration and salary levels during that period.

The Hall of Fame Factor: Lump Sum or Continued Income?

For those fortunate enough to reach the Baseball Hall of Fame, an interesting nuance often appears. Frequently, the pension payments from the MLB plan would cease, replaced by a significant lump sum payment, usually a sum equivalent to half or even two years’ worth of pension benefits. Effectively, this means the pension portion is cashed out in a single payment at the time of induction, often providing a hefty amount that players can then utilize however needed in their retirement strategy. This choice presents a stark contrast between a lifetime of guaranteed income and a substantial single payment, prompting careful consideration even before eligibility for induction is achieved.

A Deeper Dive into Payout Value: Is It Enough?

Assessing “enough” is inherently subjective and depends heavily on individual circumstances, particularly pre-retirement savings in other vehicles like 401(k)s or personal savings outside the pension plan. Historically, MLB pensions, especially in their early decades pre-stabilization, were among the highest in professional sports – significantly outpacing corporate pensions at the time. Adjustments have been made to maintain solvency, ensuring payments remain viable long-term. A typical pension might replace a significant portion of a lower-to-middle tier player’s pre-retirement earnings, though it rarely covers all expenses for a comfortable lifestyle without supplementary income or assets. High-earning players from earlier eras might have pensions exceeding their final salaries, while those of shorter tenures will naturally have lower guaranteed income. However, it’s worth noting that the pension is designed as a lifetime annuity, providing a reliable, long-term financial cushion.

Considerations Beyond Just the Payout

The pension is just one part of the financial equation for retired players. Survivor annuities are available for qualified widows or widowers, providing a portion of the player’s pension for life. Health coverage through the Major League Baseball Players Association (MLBPA), often called the “Pension Plan Healthcare” or “PPH,” is another critical component frequently funded by ongoing assessments on team revenues, providing health insurance coverage for retirees.

Potential Shocks and the Need for Prudence

While the pension provides undeniable stability and peace of mind, relying exclusively on it without a diversified retirement portfolio is fraught with peril. Life expectancy, potential health issues requiring significant savings for long-term care, and unanticipated family needs can strain even the most secure pension income. Inflation is another silent factor; while the pension amount is fixed (or indexed minimally, depending on specific plan rules), it often doesn’t keep pace perfectly with inflation, potentially eroding purchasing power over decades.

Closing Thoughts: A Defined Future, But Is It Sufficient?

The intricacies surrounding the MLB Pension Plan reveal a commitment to providing a secure financial foundation for retired players, rooted in a structured, dedicated funding source unlike many corporate offerings. Knowing the mechanics can demystify the payouts. While the structure answers the core question – yes, significant sums were, and still are, promised – the actual figure varies, and context is key. It’s a defined benefit, offering predictability, but participants must still think critically about whether this sole stream, coupled with potential health benefits, will truly support the lifestyle they anticipate in retirement. The legacy is there, the promise is kept, but a full financial picture requires looking beyond the headline figure to the entire retirement landscape.